Newsroom

Risk-based pricing notice requirements explained in Compliance Monitor

The latest edition of NAFCU's Compliance Monitor provides an in-depth overview of the Fair Credit Reporting Act's (FCRA) requirement related to sending risk-based pricing notices to consumers. The Monitor – a free, member-only benefit – is now available for download.

The latest edition of NAFCU's Compliance Monitor provides an in-depth overview of the Fair Credit Reporting Act's (FCRA) requirement related to sending risk-based pricing notices to consumers. The Monitor – a free, member-only benefit – is now available for download.

Also included in the new Monitor is an update on the IRS's clarification that Form 4720 – a form federal credit unions must submit related to the new excise tax on excess executive compensation – is not subject to public disclosure unless filed by a private foundation.

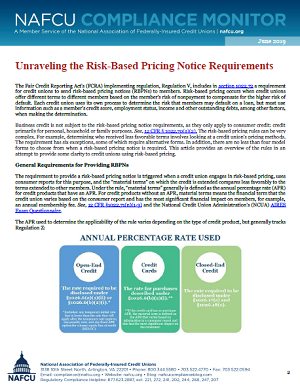

In the article on risk-based pricing, Alma Calcano, NAFCU's regulatory compliance specialist, provides resources and graphics to break down the notice requirement's rules. Calcano notes that the requirements kick-in when credit unions offer different terms to different members based on the member's risk of nonpayment to compensate for the higher risk of default.

"The risk-based pricing rules can be very complex. For example, determining who received less favorable terms involves looking at a credit union's pricing methods," writes Calcano. "The requirement has six exceptions, some of which require alternative forms. In addition, there are no less than four model forms to choose from when a risk-based pricing notice is required."

Calcano further explains the six exceptions, which are related to:

- specific terms;

- adverse action notice;

- prescreened solicitations;

- loans secured by residential real property;

- other extensions of credit; and

- credit score not available.

This edition's Compliance Forum answers questions on prepaid rule requirements and mortgage interest reporting, among other topics.

Download the newest Compliance Monitor here. More of NAFCU's award-winning compliance resources can be found here.