Newsroom

Revised Q2 GDP estimate confirms COVID-19's economic downturn

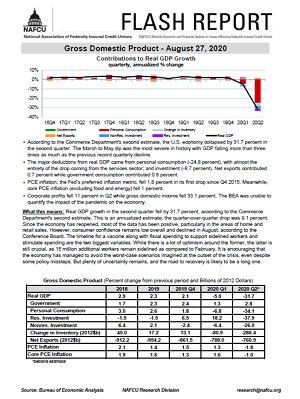

The Commerce Department Thursday released its second estimate of economic activity for the second quarter, which showed a 31.7 percent collapse due to the coronavirus pandemic. A new NAFCU Macro Data Flash report highlighted that "the March to May dip was the most severe in history with GDP falling more than three times as much as the previous recorded quarterly decline."

The Commerce Department Thursday released its second estimate of economic activity for the second quarter, which showed a 31.7 percent collapse due to the coronavirus pandemic. A new NAFCU Macro Data Flash report highlighted that "the March to May dip was the most severe in history with GDP falling more than three times as much as the previous recorded quarterly decline."

"Since the economy has reopened, most of the data has been positive, particularly in the areas of home and retail sales," said Curt Long, NAFCU's chief economist and vice president of research. "However, consumer confidence remains low overall and declined in August, according to the Conference Board.

"The timeline for a vaccine along with fiscal spending to support sidelined workers and stimulate spending are the two biggest variables," Long added. "While there is a lot of optimism around the former, the latter is still crucial, as 15 million additional workers remain sidelined as compared to February."

According to the estimate, major deductions from real GDP came from personal consumption (-24.8 percent) – almost entirely in the services sector – and investment (-8.7 percent). Net exports contributed 0.7 percent, and government consumption contributed 0.8 percent.

PCE inflation, the Fed's preferred inflation metric, experienced its first drop since the fourth quarter of 2015, falling 1.8 percent. Meanwhile, core PCE inflation, excluding food and energy, fell 1 percent.

"It is encouraging that the economy has managed to avoid the worst-case scenarios imagine at the outset of the crisis, even despite some policy missteps. But plenty of uncertainty remains, and the road to recovery is likely to be a long one," Long concluded.