Newsroom

NAFCU details NCUA PPP rules in new alert to CUs

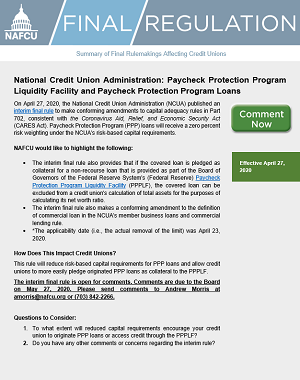

Earlier this month, the NCUA Board approved an interim final rule to make conforming amendments to capital adequacy rules consistent with the CARES Act. Under the rule, paycheck protection program loans will receive a zero percent risk weighting under the NCUA's risk-based net worth requirement. NAFCU outlines what credit unions should know regarding the rule in a new Final Regulation Alert.

Earlier this month, the NCUA Board approved an interim final rule to make conforming amendments to capital adequacy rules consistent with the CARES Act. Under the rule, paycheck protection program loans will receive a zero percent risk weighting under the NCUA's risk-based net worth requirement. NAFCU outlines what credit unions should know regarding the rule in a new Final Regulation Alert.

NAFCU has previously urged the agency to grant additional capital flexibility, as well as place a moratorium on exams, and more, and will continue to advocate for additional relief and guidance.

In the alert, NAFCU highlights that the rule:

- provides that if a PPP loan is pledged as collateral for a non-recourse loan that is provided as part of the Board of Governors of the Federal Reserve System's Paycheck Protection Program Liquidity Facility (PPPLF), the pledged loan can be excluded from a credit union's calculation of total assets for the purposes of calculating its net worth ratio; and

- also makes a conforming amendment to the definition of commercial loan in the NCUA's member business loans and commercial lending rule.

The alert also details how the change impacts credit unions and provides a general overview. NAFCU would like to know to what extent reduced capital requirements encourage credit unions to originate PPP loans or access credit through the PPPLF, as well as any other comments or concerns regarding the interim rule.

Additionally, the NCUA Tuesday released a new Letter to Credit Unions discussing regulatory considerations related to the PPP and providing clarifications on PPP loans to credit union officials and non-members based on guidance from the Small Business Administration.

The interim final rule became effective on April 27, and is currently open for comments. Comments are due to the NCUA May 27, credit unions who wish to comment are encouraged to send comments to NAFCU Senior Counsel for Research and Policy Andrew Morris.