Newsroom

NAFCU Shares Why CDFIs Play Vital Role in Helping Underserved Communities

WASHINGTON - National Association of Federally-Insured Credit Unions (NAFCU) representative Jeanne Kucey, President and CEO of JetStream Federal Credit Union (Miami Lakes, Fla.), will testify on behalf of the association at today’s Senate Banking Subcommittee on Financial Institutions and Consumer Protection hearing on the role of developmental financial institutions (CDFIs) and minority depository institutions (MDIs) in their communities. Of note, Kucey JetStream Federal Credit Union is a low-income CDFI and MDI credit union. The hearing, entitled “The Role that Community Development Financial Institutions and Minority Depository Institutions Serve in Supporting Communities,” will begin at 2:30 p.m. Eastern.

“Credit unions are also proud of their participation in the CDFI program, which provides grants to allow credit unions to better serve low-income members and underbanked communities. There were 416 CDFI-designated credit unions as of December 28, 2021, up from 285 in November of 2018, serving nearly 17 million predominantly low-income consumers and communities of color,” said President and CEO of JetStream Federal Credit Union Jeanne Kucey.

NAFCU has advocated for increased funding for CDFI’s, noting that the programs have been an "invaluable means of providing financial services to underserved areas." The association has also supported legislation like the CDFI Bond Guarantee Program Improvement Act, introduced by Housing, Transportation, and Community Development Subcommittee Chairwoman Tina Smith, D-Minn., and Ranking Member Mike Rounds, R-S.D., which aims to jumpstart economic development in economically distressed areas and address disparities in access to capital for underserved communities by strengthening and expanding.

In addition, NAFCU has called on the Treasury Department to address the CDFI backlog, requesting enhanced transparency and communication on pending applications for credit unions seeking CDFI certification. Vice President of Regulatory Affairs Ann Kossachev expressed concerns around the backlog and application process a writing that a “failure to be forthright with applicants can result, and is currently resulting, in applicants becoming disillusioned with the application process, and potential applicants becoming hesitant to enter a complicated and costly endeavor with an indefinite end date.”

***

Testimony of

Jeanne Kucey

Chief Executive Officer

JetStream Federal Credit Union

On behalf of

The National Association of Federally-Insured Credit Unions

“The Role that Community Development Financial Institutions and Minority Depository Institutions Serve in Supporting Communities”

Before the

Senate Banking Subcommittee on Financial Institutions and Consumer Protection

February 9, 2022

Introduction

Good afternoon, Chairman Warnock, Ranking Member Tillis, and Members of the Subcommittee. My name is Jeanne Kucey, and I am testifying today on behalf of the National Association of Federally-Insured Credit Unions (NAFCU), where I served on the Board of Directors for 9 years including the final two years as Board Chair. I currently serve as CEO of JetStream Federal Credit Union, a low-income designated Community Development Financial Institution (CDFI) operating in Miami-Dade County, Florida, and Puerto Rico. We are also classified as a Minority Depository Institution (MDI). Thank you for holding this important hearing today. We appreciate the opportunity to share our views on the important role that CDFIs and MDIs play in the economy and our communities. In addition to our testimony, NAFCU member credit unions look forward to continuing to work with you beyond this hearing to ensure access to robust financial services products for all Americans.

Founded in 1948 and headquartered in Miami Lakes, Florida, JetStream FCU has $240 million in assets and serves more than 18,000 members in five locations, including one in Puerto Rico. Membership is open to those who live or work in Miami-Dade County, Florida, or in Carolina, Trujillo Alto, or San Juan, Puerto Rico. Today, the credit union offers a variety of products, including checking and savings accounts, credit cards, auto loans, home equity lines of credit, business loans, several types of green loans, and no credit check loans. We also offer a complete menu of remote services through mobile banking and various digital channels.

Background on Credit Unions

Credit unions serve a unique function in the delivery of necessary financial services to Americans. Established by an act of Congress in 1934, the federal credit union system serves to promote thrift and make financial services available to all consumers, many of whom would otherwise have limited access to financial services. Every credit union is a cooperative institution organized “for the purpose of promoting thrift among its members and creating a source of credit for provident or productive purposes” (12 § USC 1752(1)). Congress established credit unions as an alternative to banks and to meet a precise public need, and today credit unions provide financial services to over 127 million people. Since President Franklin D. Roosevelt signed the Federal Credit Union Act (FCU Act) into law nearly 88 years ago, two fundamental principles regarding the operation of credit unions remain every bit as important today as in 1934:

1. Credit unions remain totally committed to providing their members with efficient, lowcost, personal financial services; and,

2. Credit unions continue to emphasize traditional cooperative values such as democracy and volunteerism.

The nation’s approximately 5,000 federally-insured credit unions serve a different purpose and have a fundamentally different structure than traditional banks. Credit unions exist solely for providing financial services to their members, while banks aim to make a profit for a limited number of shareholders. As owners of cooperative financial institutions, united by a common bond, all credit union members have an equal say in the operation of their credit union—“one member, one vote”—regardless of the dollar amount they have on account. These singular rights extend all the way from making basic operating decisions to electing the board of directors, something unheard of among for-profit, stock-owned banks. Unlike their counterparts at banks and thrifts, federal credit union directors generally serve without remuneration, epitomizing the true volunteer spirit permeating the credit union community.

Credit unions continue to play a very important role in the lives of millions of Americans from all walks of life. Since the Great Recession, consolidation of the commercial banking sector has progressed at an increasingly rapid rate. At a time when for-profit banks are deemphasizing the human touch for financial services, credit unions are second-to-none in providing their members with quality personal financial services at the lowest possible cost.

Credit Unions as MDIs, CDFIs

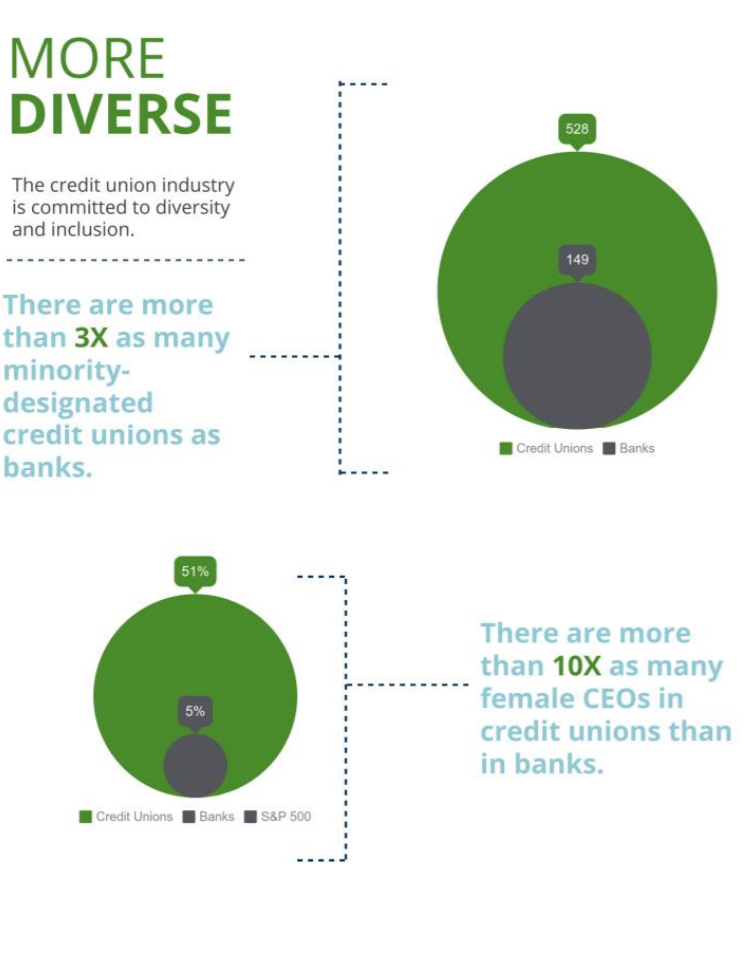

Credit unions are proud of their record of diversity. As you can see from the charts on the next page, credit unions outpace banks when it comes to MDIs and in having female CEOs. According to NCUA’s “2020 Minority Depository Institutions Report to Congress,” at the end of 2020 there were 520 federally-insured credit unions designated as MDIs, 417 of which also have the lowincome credit union designation. Credit union MDIs are located in 37 states, Washington, D.C., Puerto Rico, and the U.S. Virgin Islands. These institutions serve over 4.3 million members and tend to be smaller institutions; 82 percent of MDI credit unions have assets of $100 million or less. They also tend to underperform growth in all categories, including asset size, membership, and loan volume, in comparison to the rest of the credit union industry, and the disparity is growing.

Credit unions are also proud of their participation in the CDFI program, which provides grants to allow credit unions to better serve low-income members and underbanked communities. There were 416 CDFI-designated credit unions as of December 28, 2021, up from 285 in November of 2018, serving nearly 17 million predominantly low-income consumers and communities of color. In addition to helping credit unions in low-income areas serve members in need, the CDFI program gives credit unions access to funds that they are not able to raise from the capital markets. As the country continues its pandemic recovery, NAFCU urges Congress to consider increased funding levels for CDFI programs in any future Fiscal Year appropriations bills. It is this program that gives credit unions like JetStream an important resource to help create programs to serve their communities.

Furthermore, while Congress is considering support for the CDFI funds, we urge you to ensure that the Treasury Department is given the necessary resources to clear out the current CDFI application backlog. As the number of credit unions applying to become CDFI designated institutions continues to grow, many applicants have seen the application process drag on as they await approval. NAFCU also supports legislative measures to streamline and modernize the requirements and application process to make it easier for institutions to be approved as a CDFI.

JetStream FCU’s Role as an MDI/CDFI

In 2011, JetStream became an NCUA designated low-income credit union, and a year later became CDFI certified. We were the first credit union to service both Miami-Dade County, FL, and Puerto Rico to do so. We are heavily vested in the prosperity of the communities we serve. We have supported our members during hurricanes, government shutdowns, and most recently during the COVID-19 pandemic. Since 2011, JetStream has received $5.8 million dollars in CDFI grants to support a plethora of programs, including small business lending and a resettlement loan program for low-income members. The grants also supported the Whole Again loan program, an initiative that provided $17 million in consumer loans to replace goods and vehicles destroyed by Hurricanes Irma and María. In 2021, JetStream was awarded a grant to fund green energy and home rehabilitations. Since 2014, we have worked to ensure that every person employed at JetStream, including interns, receive certification in Community Development Certified Financial Counseling from the National Cooperative Business Association. This program trains our staff to identify financial distress within our membership and proactively work to prevent financial catastrophe.

Our membership is diverse, and reflective of the communities Jetstream serves:

• 71 percent of JetStream members are classified as low-income or below;

• 40 percent are classified as extremely low income;

• 67.5 percent of our members are Hispanic (27 percent of which are Puerto Rican)

• 18.8 percent of our membership is African American.

JetStream is also a “Juntos Avanzamos” credit union (“Together We Advance”), which is a community of credit unions committed to serving and empowering Hispanic communities. We were the first credit union in Florida to receive such a designation. JetStream is committed to meeting the needs of our members, and that has led us to offer a number of products to help immigrants and those with lower incomes, such as a second chance checking program, low dollar loans, and even a resettlement loan program for those moving from Puerto Rico to the mainland.

Jetstream, along with NAFCU, regularly works with Inclusiv, a certified CDFI intermediary and a national network of nearly 450 CDFI certified and minority designated credit unions. Inclusiv provides capital, makes connections, builds capacity, develops innovative products and services for community development credit unions (CDCUs).

Due to the geographical areas JetStream services, Hurricane Irma and Hurricane Maria critically affected our membership in September 2017. The two Hurricanes were a life-defining moment for many of our members, and we knew that we had to act. JetStream provided $2.5 million of critical financial relief to our members during the first eight months of recovery, including no-cost, zero percent APR short-term loans, deferment of existing loan payments, elimination of transactional fees, and financial coaching for our members who were dealing with active insurance cases and attempting to rebuild their homes.

We played a big role for our members with small businesses after the hurricanes. When Hurricane Maria hit the island of Puerto Rico, almost every household was affected. During this time, residents looked for ways to help their neighbors. One of our members saw the necessity on the island for accessible diesel gas to refuel generators in people’s houses. He and his wife bought a truck in the states and brought it to the island to start their new business, Chester Energía y Transportes. He worked with the credit union to open a business account to help their business get off the ground. Due to high demand, their business took off rapidly and they were able to assist other large and small businesses.

When the COVID-19 pandemic hit, Jetstream decided that the credit union’s branches would stay open. By strictly following CDC guidelines, we were able to keep our employees safe while serving our membership in their time of need. Jetstream maintained normal operating hours throughout the crisis. This also meant support for members of other credit unions through shared branching. Jetstream’s shared branching activity skyrocketed, earning recognition from Florida Credit Union Shared Services in their annual report.

In 2020, Jetstream launched a multipronged COVID-19 emergency relief program that included emergency loans, lines of credit, a 6-month payment deferral for qualifying loans, and fee waivers. Consumer loan deferments totaled 1,291, for a total of $10.5 million, and fee income was reduced by 32 percent. Jetstream saw a reduction of $348,011 to its net income. Net income for 2021 was positive, but not quite back to pre-pandemic levels. For us, this was an investment in our members during their time of need. I am proud of our team and their dedication to serve our members.

Our low-income members are more likely to live in urban heat islands with fewer trees and more pavement, as well as reside in housing with older building materials and appliances. In Miami, 65 percent of the housing stock is over 50 years old. As a result, there is a huge need for major repairs and retrofitting such as new roofs, installing impact windows, performing mold remediation, replacement of air conditioning units, and making energy-efficient upgrades. While our current Home Equity Credit Line product enables many of our members to finance these repairs, we have identified a segment of our membership that does not qualify for this type of loan due to a lack of equity, poor credit history, or high debt ratios. They are trapped in older, energy inefficient homes that are often in dire need of substantial repairs.

Our answer was JetStream’s Increasing Climate Resiliency and Health Equity through Energy Efficiency (ICRHEEE) strategy, and we are fortunate to have recently been approved for a CDFI grant for this program. The ICRHEEE addresses these challenges with innovative Green Loan products and underwriting created to improve energy efficiencies for low-income homeowners and also help those who need major repairs to their homes, resulting in improved housing stock and increased household income. This strategy includes loan options that do not require equity and are lenient with respect to debt ratios and poor credit. The strategy also includes financial counseling, coaching, and community outreach. We are looking forward to unveiling these new products and services to our members in 2022 in an effort to meet more of the needs of our membership and the local community.

Energy costs have been rising across the U.S. and these rising costs have a disproportionately high impact, also known as energy burden, on low- and moderate-income (LMI) communities and communities of color. These are precisely the communities that have not had equitable access to financing critical energy efficiency and clean energy building upgrades that could ease this energy burden. As financial cooperatives committed to investing in strong and healthy communities, CDFIs, like JetStream, are uniquely poised to serve as vehicles to deploy affordable green loan programs that combat climate change while helping to lower the high energy burden on low- and moderate-income and communities of color. CDFI credit unions have the underwriting expertise and financial coaching capacity to reach a broad range of consumers and to connect the benefits of clean energy to household budgets.

As we work to address this, and as part of our involvement with Inclusiv, we have sent our lending team through their Solar Finance Training Program for CDFIs and other community-based lenders. In this training, CDFIs design and launch affordable green loan products for their communities – something we will bring to our ICRHEEE strategy.

Recommendations

As the Subcommittee examines approaches to aid CDFIs and MDIs, we believe it is important to properly fund federal support for CDFIs and MDIs. This includes increased funding through the annual appropriations process for both the CDFI Fund and the NCUA’s Community Development Revolving Loan Fund (CDRLF). The CDRLF is an important tool for credit unions to serve lowincome areas by providing grants to low-income credit unions to meet needs in those areas, often to provide technology resources to help members. During the pandemic, CDRLF requests have far outpaced available funding. NCUA Chairman Todd Harper has specifically called for additional CDRLF funding to help low-income credit unions.

Additionally, we would support creating a CDFI Crisis Fund that would automatically make additional capital available to CDFIs to address natural disasters and economic crises when they occur in their community as proposed by Senator Brian Schatz.

Finally, we would urge you to consider the following areas to assist CDFI and MDI credit unions:

Improve the Process for Certification as a CDFI

As noted earlier in my testimony, NAFCU has heard from many credit unions that have been waiting several months for certification as a CDFI with little clarity or insight on their status. While it is important that the CDFI Fund have the resources to handle the volume of applications in a more timely manner, it is also critical that technical issues or overburdensome requirements do not hamper efforts by credit unions to serve those who want to help members in need. We believe that the CDFI Fund is best situated as a resource for institutions, and not a regulator. Additionally, transparency is key. As such, we believe the process for certifying, and maintaining certification, for a credit union, as an insured depository institution (IDI), should recognize our unique nature. Examples of how this can be done include:

• Ensuring that the “primary mission test” is not a hurdle for credit unions as not-for-profit member-owned cooperatives;

• The “target market test” for certification should focus on those to whom the credit union provides a wider range of financial services, and not just to whom it has already made loans, to meet thresholds; and

• Allowing a longer “cure period” to maintain certification that ensures credit unions can keep existing CDFI-backed programs in place. Credit unions, as not-for-profit, memberowned financial institutions, often face limited resources and staffing, which may impact their ability to quickly cure any issues, but they are still required to meet the same regulatory burdens and subject to the same market pressures as large, for-profit banks. A longer “cure period” for CDFI credit unions will allow us to meet the challenges of unforeseen events like natural disasters and pandemics—and deal with existing regulatory requirements, some of which are unique to credit unions—all while continuing to serve our communities.

Allow all Credit Unions to Serve Underserved Areas

As has been noted by Members of Congress across the political spectrum, credit unions were not the cause of the Great Recession, and an examination of their lending data indicates that credit union mortgage lending outperformed bank mortgage lending during the downturn. This is partly because credit unions did not contribute to the proliferation of subprime loans. Before, during, and after the financial crisis, credit unions continued to make quality loans through sound underwriting practices focused on providing their members with solid products they can afford.

In addition, both during and after the crisis, credit unions have been committed to helping the portions of their communities that are most in need obtain high quality products and services. This has been demonstrated once again during the pandemic. Unfortunately, credit unions that want to do more are limited in who they can serve by the FCU Act, which restricts credit unions to serving a distinct field of membership. Many credit unions want to help those in underserved areas but the ability to add underserved areas to their fields of membership is limited. Currently, only multiplecommon-bond credit unions have the authority to add underserved areas. We urge the Committee to amend the FCU Act to allow all credit unions the ability to add underserved areas to their fields of membership.

Loan Maturity Limits

The FCU Act has a general statutory limit on federal credit union loans of 15 years, with a limited number of exceptions, such as mortgage loans for a primary residence. The rigid and limited set of exceptions to the FCU Act’s general 15-year maturity limit does not provide the NCUA with the ability to expand the types of loans that may be made with a longer maturity limit through regulation. For example, many military members may purchase a home to move to when their service ends, but because it is not their current primary residence, they may be unable to obtain a loan with a term longer than 15 years. Additionally, a number of credit unions have been approached by members wanting to obtain financing for solar loans with a longer term to make the loan more affordable. Both of these examples highlight the fact that the current 15-year limit is outdated and does not conform to maturities that are commonly accepted in the market today, resulting in credit unions turning away members in need and losing market share in a growing area of climate-friendly lending. In a rising interest rate environment, it is important that consumers have options for longer maturity products. We urge you to support S.762, the Expanding Access to Lending Options Act, introduced by Senators Tim Scott, R-SC, and Catherine Cortez-Masto, DNV, to address this issue.

Allow GSEs to Purchase Non-Conforming Loans from CDFIs

An important aspect of the CDFI Fund is that it provides awards to CDFI institutions to allow them to finance mortgage lending for first-time homebuyers and be able to provide flexible underwriting for community facilities. CDFIs often provide educational services such as credit counseling and homebuyer classes to help their borrowers use credit effectively and ensure they are able to keep up with their loan obligations. However, the majority of the mortgages originated by CDFIs are considered non-conforming (as they do not meet the loan-to-value, debt-to-income, FICO score, or other requirements), and Fannie Mae and Freddie Mac (the government-sponsored enterprises (GSEs)) are unable to purchase these loans. NAFCU has urged the Federal Housing Finance Agency (FHFA) to create a pilot program to allow the GSEs to buy such non-conforming loans from CDFIs because they are serving the exact communities that the GSEs aim to serve through their statutorily mandated missions.

Credit unions that are classified as CDFIs are best situated to originate loans to the communities most in need. NAFCU believes that one way to help address the widening homeownership gap for minorities would be for the FHFA to permit the GSEs to purchase mortgages like the ones made by CDFIs to their communities through new pilot programs with less stringent purchase criteria. Establishing such pilot programs will facilitate the development of a vibrant secondary market, thus ensuring the long-term viability and even expansion of such lending programs in the primary mortgage market. This would mean CDFIs could make more of these loans to support their communities and help resolve some of the access and equity issues currently impacting many borrowers. Should the FHFA prove unwilling to allow the GSEs to purchase these mortgages, we urge you to consider taking legislative action on behalf of CDFIs and the underserved areas they serve to bring about this change.

Federal Housing Administration (FHA) Lending

Credit unions in general, and especially credit unions designated as CDFIs and MDIs, play a vital role in supporting underserved communities. As noted above, to obtain and maintain their certification, CDFIs must demonstrate that at least 60 percent of their lending activity is directed to one or a combination of target markets: economically distressed geographies (Investment Areas); low-income targeted populations (LITP) and minority communities, specifically African Americans, Hispanics, and Native Americans (other targeted populations -OTP). One of CDFIs’ most important values to these communities is their ability to provide responsible and affordable mortgage lending for first-time homebuyers, lending to small businesses, and offer flexible underwriting for community facilities. The financial products offered by CDFIs are designed to support the specific needs of the borrower, particularly low- and moderate-income, as well as minority borrowers, as most are fixed-rate and self-amortizing with lower origination fees. This keeps payments affordable and allows borrowers to decrease the principal, so the loan is actually paid off at the end of the term. Although these products provide much-needed credit in their respective communities, their specialized nature may set them apart from conventional mortgage products. NAFCU has urged the Federal Housing Administration (FHA) to introduce additional 12 programs that provide insurance for CDFI loans and that make it easier for these communities to have access to FHA-backed mortgage products.

We recommend that Congress require the U.S. Department of Housing and Urban Development to conduct a study to determine the level of participation of CDFIs in FHA loan insurance programs and offer targeted training and resources to grow the number of CDFIs that are FHA-approved lenders.

De Novo Credit Unions

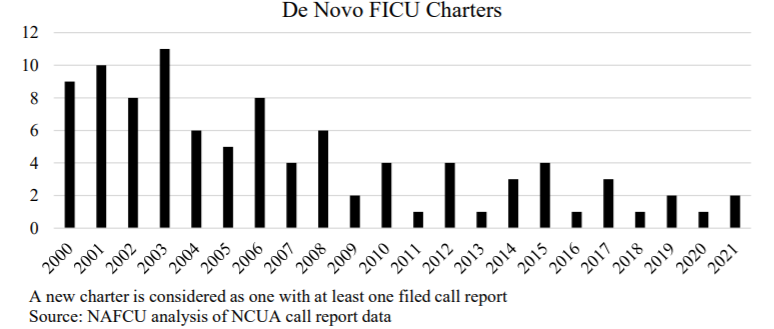

The rising cost of compliance deters many would-be de novo (start-up) credit unions. Additionally, the initial capital infusion and cash outlays are often too great for many communities and associations, and there is little to no return on investment. Starting a new credit union is essentially an altruistic endeavor, as there is no ultimate financial incentive for those that are successful, and the costs and hurdles can be discouraging. Furthermore, the complex chartering process is relatively easy and straightforward when compared to what a de novo credit union will face once it is chartered and operating. All of these factors contribute to a significant decline in the pace of de novo credit unions post financial crisis.

The chart above outlines the number of de novo federally-insured credit unions chartered since the year 2000.

The NCUA takes an active role in helping new credit unions form and provides support. NAFCU appreciates the NCUA’s strategic focus on easing barriers to the formation of new credit unions, including streamlining the chartering process, offering assistance to groups attempting to establish a new credit union in earlier stages, and providing newly formed credit unions with additional flexibility in meeting regulatory requirements.

Still, the NCUA’s abilities are limited by what is allowed under statute. NAFCU urges Congress to modernize the FCU Act to promote the chartering of de novo credit unions and to provide greater flexibility regarding prompt corrective action capital requirements for de novo credit unions. Although the FCU Act gives the NCUA the authority to offer some prompt corrective action flexibility for new credit unions, expanding the agency’s authority would be helpful.

Subordinated Debt

Congress may provide more flexibility to credit unions’ ability to serve low- and moderate-income individuals in their communities by supporting the NCUA in its efforts to permit credit unions to issue subordinated debt. Currently, low-income credit unions are able to offer a form of subordinated debt called secondary capital. Low-income credit unions may issue secondary capital accounts to non-natural persons and these accounts are generally treated as regulatory capital. The approval process to offer secondary capital can, however, be complex. NAFCU appreciates the NCUA’s recent supervisory guidance pertaining to the evaluation of secondary capital plans, as it provides valuable insight into why a secondary capital plan may be denied. Nonetheless, NAFCU continues to urge the agency to provide further support and guidance to low-income credit unions so they can better utilize this important resource.

NAFCU advocates for a more streamlined process for the approval of secondary capital applications. Although every secondary capital plan is necessarily different depending on the credit union in question, the process should be more standardized to help credit unions anticipate and better prepare their secondary capital plans for approval. Additional flexibility, guidance, and other resources, particularly on how credit unions can more comprehensively project future performance over a reasonable time horizon would be helpful as many low-income credit unions continue to face obstacles in the approval process. Additionally, NAFCU supports improved flexibility in credit unions’ capital framework to enhance consistency across regions regarding the treatment of secondary capital as it applies to a credit union’s net worth calculation.

Taking the steps outline above, as well as supporting existing proposals such as S. 3441, the CDFI Bond Guarantee Program Improvement Act offered by Senators Tina Smith, D-MN, and Mike Rounds, R-SD, would go a long way to helping meet the needs of CDFIs and allowing us to meet the challenges that arise.

Conclusion

MDIs and CDFIs play a vital role in the daily lives for millions of Americans. Preserving MDI and CDFI credit unions and fostering the development of new ones would continue to grow the financial industry as an inclusive part of the American economy.

Credit unions throughout the country are proud of the work they have done to serve minority and underserved populations. We urge the Subcommittee to support improving the CDFI experience, including regulatory relief for credit unions and support for modernizing and updating the FCU Act. Allowing established credit unions to service the communities that need the most help and providing pragmatic regulatory relief for chartering new credit unions would bring more Americans into financial institutions that put their financial well-being over profits.

Thank you again, Chairman Warnock, Ranking Member Tillis, and Members of the Subcommittee for the invitation to testify before you today. I welcome any questions you might have.

###

The National Association of Federally-Insured Credit Unions is the only national trade association focusing exclusively on federal issues affecting the nation’s federally-insured credit unions. NAFCU membership is direct and provides credit unions with the best in federal advocacy, education and compliance assistance. For more information on NAFCU, go to www.nafcu.org or @NAFCU on Twitter.