By George Hofheimer

On Dec. 9, 1936, Edward A. Filene addressed the School of Business Administration’s graduating class at the University of Buffalo. He started with a zinger:

"You may have supposed — those of you who are preparing for a business career — that I would speak to you out of the richness of my business experience and lay down the rule which, in that experience, I have found to be successful. But if I were to do that, it would be mostly bunk; for I got most of my business experience in a world which no longer exists. If I were to tell you how I got ahead in that world, it would not do you any good. If you want to know how to drive a modern car, you don’t go to someone who can tell you, out of the richness of his experience, the tried-and-true principles by which he once succeeded in chauffeuring a horse and buggy.”

Preparing for the future, Filene insisted, is about unlearning what got us “here.” Relying on the well-worn routes of the past may feel comfortable and provide success over the short term; however, truly dynamic leaders and organizations build their future on new and novel insights. So, let’s look into the future and examine which new and novel insights credit unions can leverage today for the benefit of their cooperative, their members and their communities.

What's on the Horizon

Filene Research Institute’s head of research, Taylor Nelms, Ph.D., and his former colleague at the University of California– Irvine, Stephen Rea, Ph.D., provide credit unions with an amazing resource in The Credit Union of the Twenty-First Century. I like to joke with this duo that we are already in the 21st century, but their task was to examine how credit unions can continue to thrive well past the 100th anniversary of the Federal Credit Union Act in 2034.

As we approach 2034, the role of credit unions in providing secure, fair access to financial services — particularly for individuals of small and moderate means — remains as important as ever. While many of the socioeconomic factors that drove the credit union system in the last century remain salient, more recent changes — especially technological innovations that have fundamentally changed how financial institutions interact with consumers — encourage us to reimagine the role that credit unions will play in the United States’ financial services landscape over the next decades.

Through a series of in-depth interviews with industry professionals, consultants and regulators, and an extensive examination of more than 100 secondary sources, the researchers imagine a not-too-distant operating and regulatory future for credit unions. The research paints a future credit union landscape that is both enabled by technology and altered by changing economic conditions and consumer attitudes. Some of the most important socioeconomic transformations include:

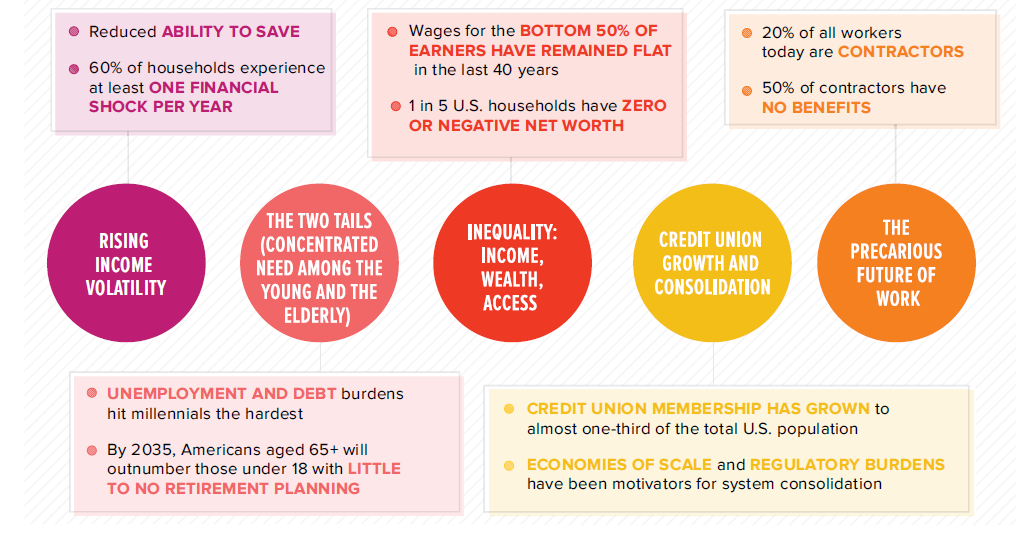

- growing income volatility and financial fragility;

- growing income and wealth inequality;

- credit union growth and consolidation;

- generational divisions, leading to what the researchers call the “two tails” problem of concentrated need among the young and elderly; and

- an increase in the proportion of precarious workers and the rise of a “1099” workforce.

For consumer preferences and expectations, some of the key drivers of changes include:

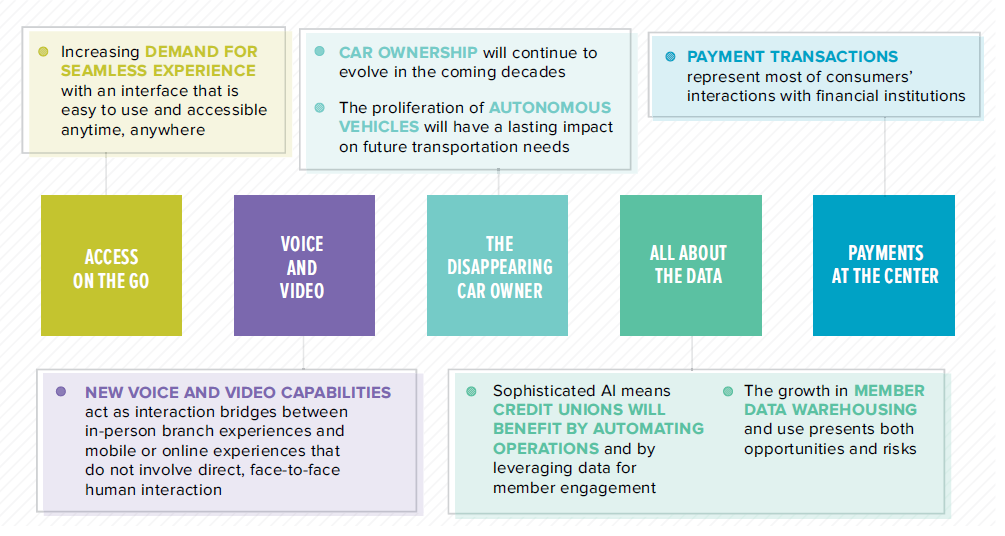

- a shift away from traditional branching delivery channels;

- significant advances in, and consumer adoption of, sophisticated voice and video capabilities;

- consumers’ changing relationships with automobiles;

- radical enhancements in data analytics and automation; and

- the emergent role of payments as the key entry point into financial relationships.

Changes in Consumer Interactions

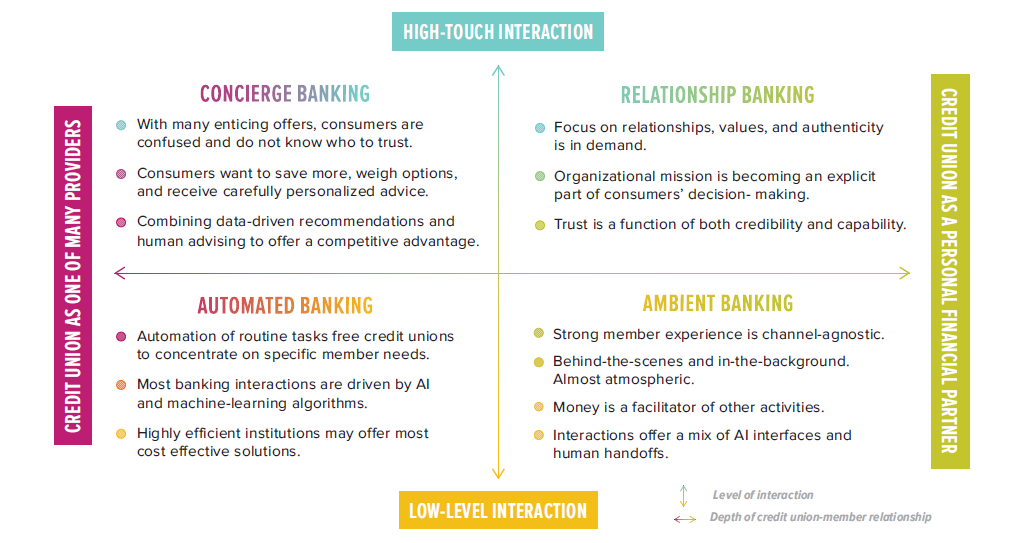

These trends result in a potentially new — and radically different — operating and regulatory model for credit unions in this century. From an operational perspective, credit unions need to adopt impactful technologies that are already changing the consumer’s relationship with their financial services provider. The authors recommend credit unions prepare for this future by developing and deepening four models for the provision of consumer financial services.

Relationship banking. This is differentiated by credit unions’ deep knowledge of and responsiveness to the needs of members and their communities. As one interviewee put it, “This is something deeper than a deposit. This is something way, way more than a transaction. This is about being a part of your community, and giving back, and helping the community not only survive, but even thrive.”

Ambient banking. “Money is just a facilitator of other activities, so don’t get in my way,” one interviewee explained. Yet this seamlessness cannot be achieved by taking separate pockets of the banking experience mobile. Instead, the credit union of the 21st century may ultimately become fully ambient, even atmospheric, combining Alexa-style voice interaction with a skillful mix of artificial intelligence-driven chatbots and human handoffs.

Automated banking. One of the key promises of data is in automating processes to smooth the member’s path through the credit union. Member data is the fuel of automation — from the robotic processing of routine tasks, to natural language processing, to more advanced decision-making and risk assessment driven by AI and machine learning. The researchers suggest that by automating large parts of financial services delivery, credit unions can concentrate on specific member needs and relationships.

Concierge banking. As the researchers explain, consumers in the early 21st century want to save more, but they are stymied by instability and uncertainty in their day-to-day financial lives. They want to improve their credit and start investing responsibly, with carefully personalized loan and investment recommendations; but when they start looking, they are confused and exhausted sorting through the numerous complex options that pop up on Google. They want good financial advice to help them plan for tomorrow and for the future, but they don’t know whom to trust. By combining data-driven recommendations and human financial advising, the 21st-century credit union can become a member’s financial concierge.

How to Grow in This Century

Regulatory structures will also have to evolve alongside operating models to enable credit union growth in the 21st century. The researchers emphasize the need to create alternative sources of capital to fuel options for growth. Inspired by their interviewees, they also begin to reimagine credit unions’ fields of membership and communal common bonds to better fit in a world that, as the researchers write, is “increasingly likely to manifest [relationships] in dynamic, digital- or virtual-world contexts.”

The researchers ask that we rethink the creation and self-definition of credit union fields of membership: “Credit unions today do not serve only preexisting communities. Rather, communities are made and maintained, in part, through participation in credit unions.”

The world is changing in exciting and unpredictable ways. This study rightfully claims credit unions need to be proactive about preparing for that uncertain future.

Edward Filene concluded his commencement speech in Buffalo by urging the University of Buffalo graduating class of 1936 “to find out how [the future] is put together.” One of the promising highlights of this research is the authors’ contention that something as “old-fashioned” as the philosophy of cooperative finance will still matter well into the technology-enabled 21st century. Much like the comfort of a physical book in today’s world of screens, that philosophy is not an anachronistic relic but a beacon that will illuminate a safe path for credit unions as they make their way into an uncertain future. Past is prologue, but maybe not in the way you think.

Access the full report, a strategic planning guidebook and slide decks associated with The Credit Union of the Twenty-First Century project.

George Hofheimer is executive vice president and chief research and development officer at Filene Research Institute.

This article was published in the March-April 2020 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content:

- The NAFCU Journal: Serving Rural America

- The NAFCU Journal: The Labor Force of Tomorrow