By Curt Long

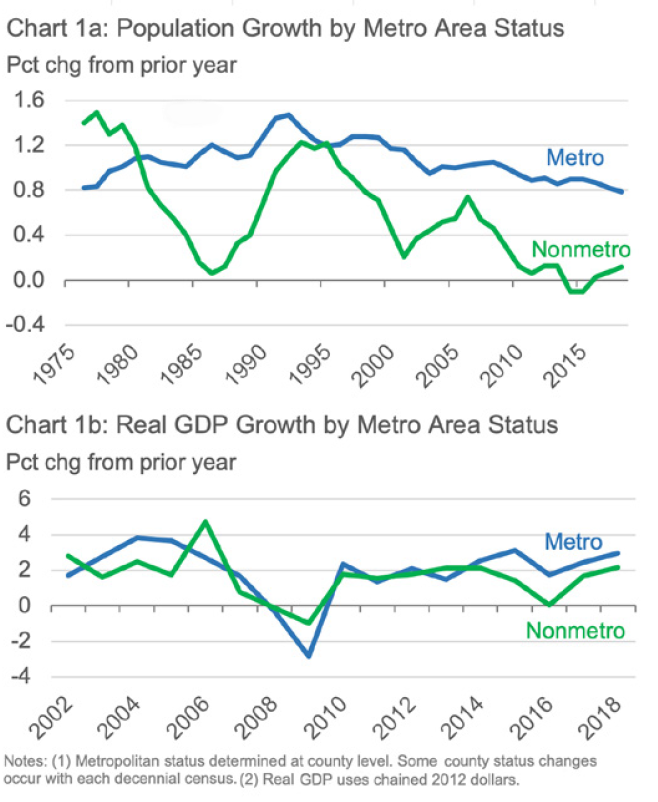

Rural areas are a frequent topic of media focus. Stories of their slow demise are abundant, citing hollowed-out factories, outmigration to urban areas and a shrinking tax base. It is true that rural population growth has been essentially flat in recent years. While there have been brief times in previous decades when that was the case, the persistently slow rural population growth of recent years is unique (see Chart 1a). The Bureau of Economic Analysis recently completed county-level GDP estimates, allowing for aggregation among urban counties (those in a metropolitan statistical area, or MSA) and rural ones. Those figures show that urban area real GDP growth has been, on average, one percentage point higher than rural GDP growth since 2013 (see Chart 1b).

These trends would appear to carry some large implications for financial institutions. A report from the Federal Reserve at the end of last year noted that the number of bank branches in rural counties declined 14 percent between 2012 and 2017. Furthermore, households in rural areas are far more likely than urban households to use branches as their primary method for accessing banking services (38 percent rural vs. 22 percent urban, according to the 2017 FDIC National Survey of Unbanked and Underbanked Households). With banks increasingly focused on denser, higher-income urban areas, credit unions are increasingly filling the gap left by their departure.

Recent Branching Trends

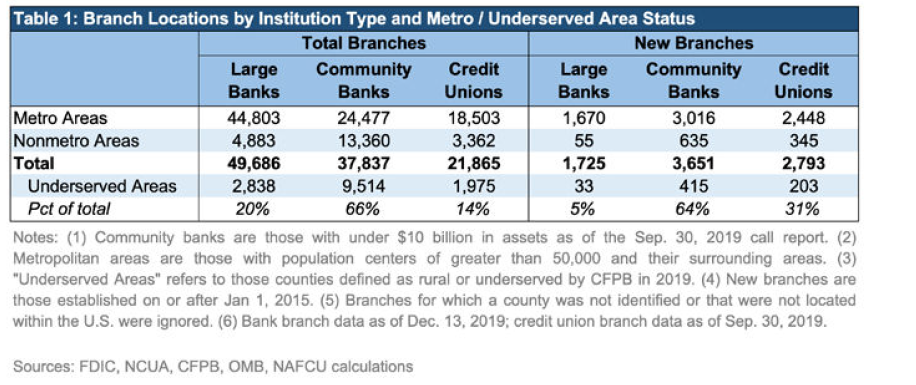

NAFCU’s analysis of branch data extends the work by the Federal Reserve by adding the type of institution. Table 1 shows that for older branches (those that have been in existence for more than five years), community banks have far greater concentrations in nonmetro areas than either large banks (those with $10 billion or more in assets) or credit unions. Metro areas host 90 percent of large banks’ older branches and 84 percent of credit unions’ older branches. However, more recently credit unions have increasingly built branches in rural counties, while banks have turned their attention to metro areas. Large banks in particular have almost completely avoided building new branches in counties outside of an MSA, with only 55 such branches built in the past five years.

These trends also mean that credit unions are playing a larger role in providing branch services to underserved areas, 98 percent of which are rural. Among older branches, credit unions account for 13 percent of total branches in those areas; but that figure jumps to 31 percent for branches built more recently. NAFCU has long argued that all credit unions should be eligible to add underserved areas to their fields of membership, regardless of their charter type. Given the lack of interest shown by banks for meeting the needs of those communities, as well as the demonstrated appetite for credit unions to expand into those areas, Congress should act to ensure that all credit unions have the ability to serve underserved areas.

Recent Credit Union Experience in Rural Areas

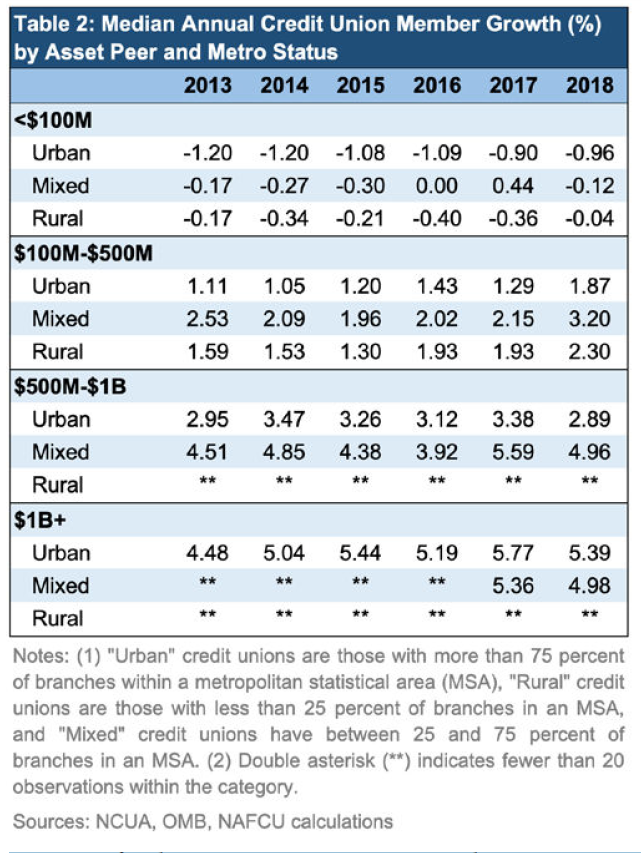

Given the broad struggles of many rural areas, they may not appear to be an inviting area for growth for a financial institution. Table 2 shows the median member growth among credit unions by asset class and metro area concentration. Perhaps surprisingly, rural credit unions (those with less than 25 percent of their branches in an MSA) have grown more quickly than urban ones (those with more than 75 percent of their branches in an MSA) at the median. This is true of both asset classes below $500 million.

While it is rarer for a larger credit union to be situated predominantly in rural areas, there are a growing number that lie in between the two extremes, with between 25 and 75 percent of their branches outside of an MSA. These “mixed” credit unions are experiencing the strongest growth rates of any category for all but the very largest credit unions. It may be that as other institutions pull out of rural areas, growth opportunities could be created for many credit unions.

As credit unions consider whether to increase their focus on rural areas, they will have to carefully assess the long-term prospects for those communities. But given the success many credit unions have found recently despite some significant headwinds, rural America may yet prove to be fertile territory for the credit union industry.

Curt Long is NAFCU’s chief economist and vice president of research.

This article was published in the March-April 2020 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content

- NAFCU’s Macro Data Flash report: Consumer Credit (member-only)

- The NAFCU Journal: The Labor Force of Tomorrow