Economists spent much of 2018 on two endeavors: looking back at the onset of the financial crisis on its 10th anniversary and pondering when the next recession would strike. Forecasting recessions is fraught with difficulties, and economists aren’t much good at it. A recent working paper from the International Monetary Fund (IMF) (Working Paper No. 18/39), which reviewed forecasts from around the globe and rated their accuracy in advance of downturns, declared public and private forecasters to be “equally good at missing recessions.”

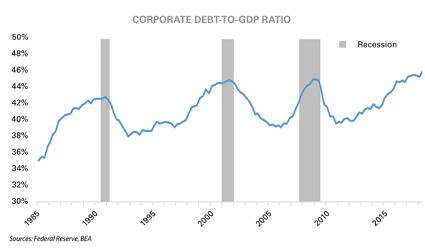

Their track record notwithstanding, a sizable faction of economists believes that recessionary risks are on the rise. In an October 2018 survey by the National Association of Business Economists, 56 percent of respondents anticipate a recession in 2020. Some of the key indicators economists are watching as they determine whether a recession is looming are: 1) the yield curve; 2) the unemployment rate; and 3) corporate debt.

The relationship between inverted yield curves and recessions is not quite an ironclad one, but it’s close. Since 1960, the yield curve has inverted eight times, and in seven of those instances a recession followed. With the spread between 10- and two-year Treasury rates narrowing recently, the relationship has been cited increasingly by observers as a factor to watch for its recessionary implications.

And yet, others are keen to say that this relationship has lost some of its predictive power in recent years. The main reason behind their skepticism is the widely held view that long-term rates are being artificially suppressed by central bank activities and investor appetites for safe assets. If that is the case, it could make inversions more likely, and the term spread’s predictive power would need to be reassessed. As far as Federal Reserve officials go, the majority seem willing to believe that an inverted yield curve may no longer mean what it used to, but there are some notable exceptions, such as St. Louis Fed President James Bullard, who are warning the Fed to slow the pace of rate hikes in order to reduce the risk of triggering a yield curve inversion.

From the January-February 2019 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.